For the benefit of all investors at this critical time in the markets, I wanted to publish an extensive excerpt of my Special Bulletin Wellington Letter from Tuesday, March 17. I don’t think our paid members will mind. They were safe during the entire crash since February 24, because of my earlier Financial Storm Begins special bulletin, published on Sunday, February 23.

I encourage you to read this several times and decide how to prevent further losses of your hard-earned savings. Ignore all the “bargain hunting” advice in the media. Many analysts in the media manage money and thus have a huge conflict of interest. I don’t and must charge for our tedious research and forecasts. “Free” can be very expensive. Enjoy the excerpt!

The Fed: Pulling Every Rabbit Out of its Hat

Stocks opened the day (March 17) higher with the DJIA up nearly 300 points at the open. That gain quickly disintegrated within 30 minutes as the index plunged to a 306-point loss. The S&P 500 approached support from the December 2018 lows, which held and helped the major indices rally higher. However, it wasn’t straight up from there.

From the open, today’s action indicated much more of a fight between the bulls and bears throughout the day. The VIX (volatility index) remained elevated near all-time highs and even hit a new record intraday high of 84.83.

By the close, the markets were able to sustain their early gains with the small-cap Russell 2000 leading the way for the first time in a number of weeks, up 6.7%. The Nasdaq and S&P 500 gained 6.3% and 6%, respectively, while the DJIA lagged all other indices with a 1048-point gain (+5.2%).

However, the internals trend that we’ve seen on other rallies continued today with all advancing internals higher but on a much smaller magnitude as the declining internals on market selloffs.

Advancing share volume was just 1.9x and 2.4x heavier than declining volume on the NYSE and Nasdaq, respectively. This shows the buying today was not very high and in fact was timid, despite the big gains in the major indices.

All 11 S&P sectors closed with gains led by the utilities sector, which crushed all others after soaring 13.1%. Consumer staples, another defensive sector, was up 8.4%, followed by real estate, up nearly 7%. There you can see the top three performing sectors were the more defensive sectors.

Energy was able to just barely close in positive territory, up 0. 7%, as WTI Crude oil fell another 6.7% to $26.80/bbl. That’s crude’s lowest price since May 2003 as it closed below the February 2016 closing price today.

The DXY dollar index jumped higher by 1.5% to 99.52, its highest level in nearly one month. The dollar is a “safe haven” which money flows into as risk appetite declines for equities.

Treasury yields jumped higher with the 10-year closing above 1% for the first time in two week to settle at 1.08%. The 30-year yield bounced to 1.68%, also a new 2-week high. This, in effect, caused the safe-haven Treasury bonds to pull back today as the TLT ETF (20+ year T-bonds) fell 6.7%.

However, looking at the volume of today’s pullback in T-bonds, we don’t see it as the start of a further decline in these as they are widely considered the safest investments in the world. There’s just too much bad news to come, and further negative data, that will greatly impact the global stock markets and economies, leading to recessions world-wide.

Commentary

Today was the day for the PPT to throw everything against the sellers and finish the day with a good up-move. Yesterday I wrote: “The chart of the S&P 500 shows that an important level is being reached, the three-month plunge low of December 24, 2018 (around 2,346). That could produce a bounce. Take some time to study this chart.”

That level was support today. In fact, the low today of the S&P 500 was just 21 points higher than my target of 2,346. Not bad for something Wall Street tells you is “impossible” to do.

Here is the chart of the S&P 500 (weekly). We are using the Heiken-Ashi chart type, which gives us the major trend.

The U.S. government is taking strong action, along with the Fed, in “Trump Time.” This administration means business. Of course, it can’t do miracles. That means the markets will now start sorting out sectors that will respond to the bailouts and those that won’t.

Then we have to reassess the governmental efforts. However, economically and financially, we are still in the early phase of the contraction and crisis. The big, important consequences are still ahead. Unemployment will soar by millions, as restaurants, bars, all sporting events, travel, etc. close down. Consider the consequences: a little short covering rally won’t erase those consequences.

Remember, the recession was starting last year. Recall the stock market “distribution,” where the majority of stocks made tops in 2018, while 1-20 stocks were pushed to new highs this year. I identified this as being the prelude to a bull trap. The VALUG index showed that the majority of stocks were being sold during that time. This was a clue that a deep, long lasting downturn was ahead.

I basically wrote that “the longer the period of distribution, the more severe the bear market and recession the follow.”

Nothing in the markets happens by coincidence. There is too much money to be made by planning the events. I wrote several times the past three years that ahead of the next election, there would be an engineered market crash and deep recession. It’s happening! We didn’t know anything about a virus at the time.

The EU today reversed itself on the disastrous policy of “‘open borders,”’ which have ruined Europe forever. It closed its borders to anyone coming in, other then EU nationals. About time! Yesterday, that would have been called “racist.” Today it is governmental policy. How fast things change.

The world won’t be the same for years. Many important countries are basically shut down. The U.S. is on its way to that. Ill-designed emergency legislation is an economic disaster.

How can politicians order restaurants and bars to shut down when many are local neighborhood places, never crowded, just serving people well known to them? Leave it to the owners. When they experience lack of customers, they will decide to close. We don’t need hysteric politicians to impose “force.”

Now we see the transitioning we wrote about: from health crisis, to economic crisis, and now the liquidity crisis. The latter is always the worst as it means potential systemic failure of the financial system. Yesterday we wrote the commercial paper market (CP) market just froze up. This often precedes a global liquidity crisis.

We are amazed that so few analysts even know the importance of that market. These are short-term “IOUs” from large companies borrowing mostly money for 90 days. These are usually rolled over when they come due. But when the market freezes, they can’t be rolled and companies have to scramble to get the billions for the ones coming due. They don’t want to default.

In the last financial crisis, Warren Buffett was the lender of last resort. He had record cash, but now has twice as much. He will now be there again. He was sitting on record cash levels of $125 billion, while he was telling people to buy stocks. He is in the driver seat again. The vulture is ready to come to the rescue…on his terms.

In late 2007 I wrote that the CP market had frozen, thus forecasting a financial crisis. The financial media paid no attention. Industrial companies have few options other than CP for short-term financing. Financial firms and banks can go to the Fed’s discount window and other liquidity sources.

Today the Fed also reinstated its commercial paper bailout facility (CPBF) from the last financial crisis. The Fed is putting $10 billion into it. In my opinion that is totally insufficient to calm fears, but it can be enlarged. It offers credit protection. The Fed said it can put $700 billion to buy CPs.

Bank of America said: “This facility does nothing to assist the money funds trying to raise cash and address outflows” implying the Fed will have to unleash another backstop.

Yes, there are many simultaneous problems. Outflow of money from MMFs (money market funds) is another. They are the biggest buyer of CP, which makes the Fed move very important. Avoid MMFs; at this point, you only want U.S. Treasurys unless it is money at a mid-size bank and guaranteed by FDIC.

My book Financial Apocalypse is a chronological account of 2008. It shows with charts what we were noticing and what Wall Street was saying at the time… there was a huge difference. For 10 years I have called this book “the guide for the next financial crisis.” Well, those who read it, now know what is likely to happen.

The Fed today did another massive liquidity injection of $500 billion into the repo market to keep it function. That’s $1 trillion in last two days. And the analysts said a month ago, “don’t worry, this (virus) is just like the flu.” That’s why their advice is “free.” Late in the day, the Fed said it would do two $500 billion injections per day. That’s $1 trillion offered per day. Panic is in the air.

Scott Minerd, managing director of Guggenheim, today said that a $2 trilllion lending facility like TARP was absolutely necessary. That was the Troubled Asset Relief Program. It allowed the government to buy bad assets (loans and bonds) from financial institutions so that they could make new loans initiated in the last crisis.

I believe that something like TALF, (Term Asset-Backed Securities Loan Facility), also started in prior crisis, may also be discussed. It encourages the issuance of securities backed by privately originated loans to consumers and businesses and to improve market conditions for ABS (asset backed securities.)

The Fed issued non-recourse loans with a term of up to five years to holders of eligible ABS. This is one way to provide money where it is needed, guaranteed by the Fed.

Late News

After the close, we heard that the Fed had created the “PDCF” facility for overnight and term funding of up to 90 days for a broad range of assets for “primary dealers.” It’s called the “Primary Dealer Credit Facility.” This is a revival of the program from the last crisis.

Primary dealers are the big financial firms that are authorized to buy Treasury securities at the Treasury’s auctions. The goal seems to be to assure that the Treasury auctions are well bid by assuring dealers a financing of what they buy. When the Treasury has to raise trillions of dollars to finance all that is coming, it needs the help of primary dealers to peddle all that confetti. Good idea!

This is the ‘big bazooka’ in the PDCF. It says: “Credit extended to primary dealers under this facility may be collateralized by a borad range of investment grade debt securities, including commercial paper and municipal bonds, and a broad range of equity securities.”

This means that stocks can now be used as security for loans from the Fed.

What’s next, ETFs and mutual funds? The Bank of Japan owns over 70% of the stocks in Japan via ETFs. That’s how they support their stock market. Could this replace the buybacks in the U.S. which vanished suddenly?

With a business person as the current president there may be better and more effective programs than during the last crisis, although we like some of these. But that won’t guarantee a good stock market. Remember, after the big TARP was passed in October 2008, the markets declined another 4 months.

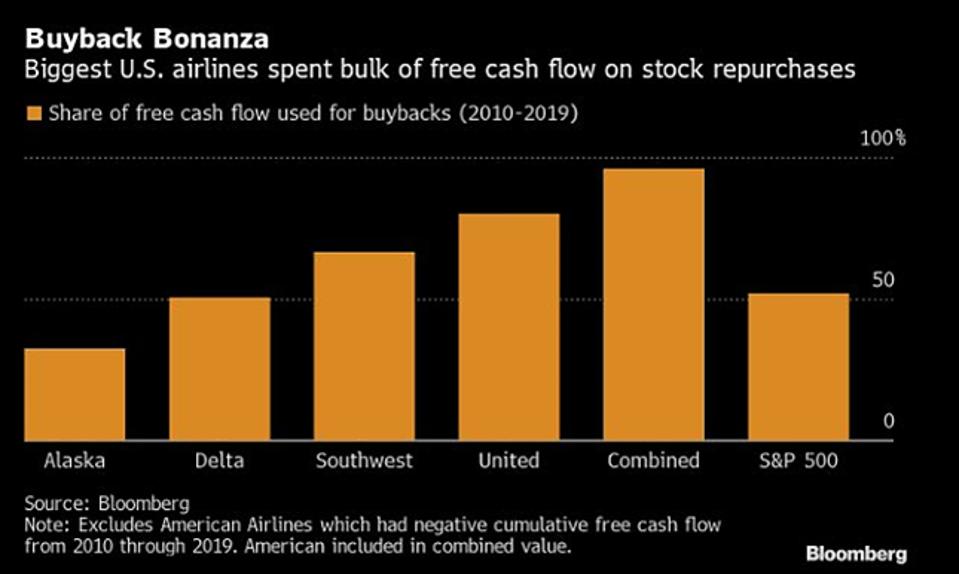

Now we see the terrible consequences of the self-enriching stock buyback programs. Mark Yusko wrote that “The biggest U.S. airlines spent 96% of free cash flow last decade buying back their own shares.” Now they have to be bailed out with the money of prudent taxpayers.

Years ago buybacks were illegal. Governments should force them to issue shares for the money and for the executives to return the profits on their stock option. See the chart below via Bloomberg of the airlines’ buybacks over the past ten years.

Anyone who thinks that all these new bailouts will have a durable positive effect on the stock market is naïve. As we pointed out for several years, the “only” big buyer of stocks the past 11 years were companies buying their own shares. We showed the charts numerous times.

Now that big buyer is out of the market, for a long time. You don’t need to be a rocket scientist to know what happens when the only big stock buyer disappears.

Conclusion

I believe that even when the virus crisis is resolved, the economic recession that actually would have occurred anyway will continue.

I think the evidence indicates that the hysteria now, much fabricated by the politicians at state levels, is much worse than the disease. It is highly contagious, but not that deadly. Based on the official “infection” numbers, fatalities are around 2%-3% of infected.

But most infected people have not been found because of lack of tests. Therefore, the actual number of infected could be 10 times higher. That would mean a fatality rate 1/10th of the above. And for that we paralyze the entire country?

I predict that eventually data will show the flu is much more deadly.

(end of excerpt)

March 18, 2020:

Today the DJIA plunged another 2,300 points again at its low. But this plunge is much, much more serious. The critical low of December 24, 2018 was broken decisively on the S&P 500 as we had forecast. The much more important VALUG index did the same last week. Many stocks of large companies are down 30%-40% today, in just one day. The word “crash” comes to mind.

Now the entire “Trump Bull Market” has been wiped out by the important indices. Next up: the entire economic growth will be wiped out. This fulfills our forecast of three years ago. Stay tuned!

Wishing you good health and prosperous investing,

Bert Dohmen, Founder

Dohmen Capital Research

Dohmen Strategies, LLC