The most often asked question of analysts in the media is whether this is a new bull market. The majority seems to be saying it is. We at Dohmen Capital Research are on the opposite side of that debate.

Investors are being told that the S&P 500 gained over 20% from the bottom of last year and that therefore, this is a “new bull market.” In our opinion, that is false! There is nothing magic about 20%.

Don’t believe everything you hear. Our motto is: “Don’t trust until you verify.”

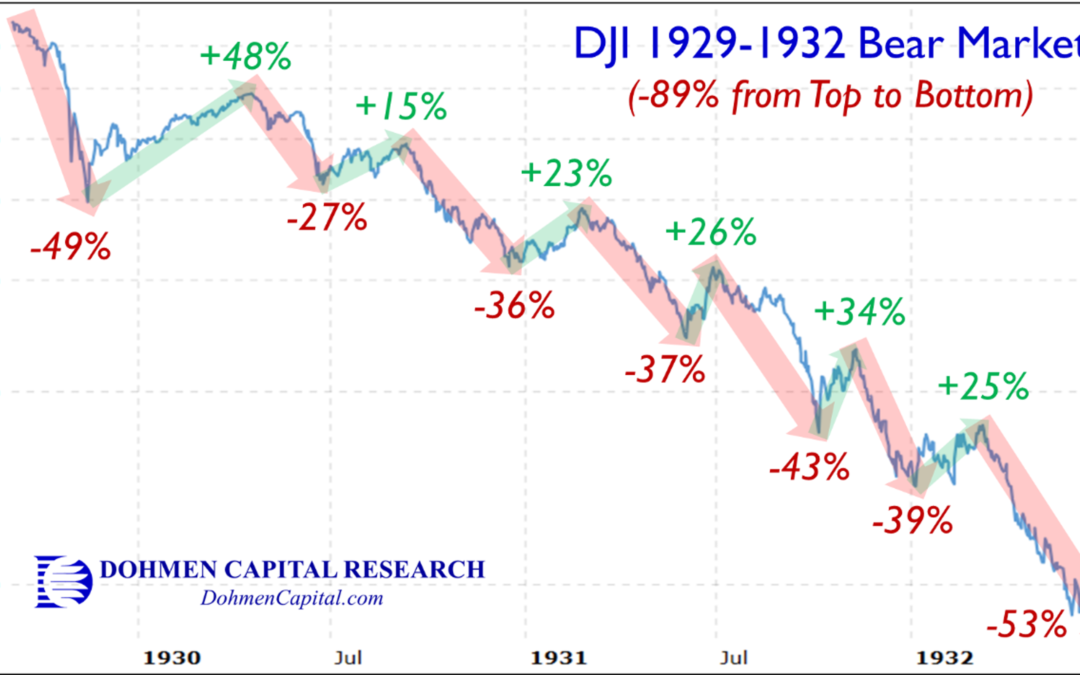

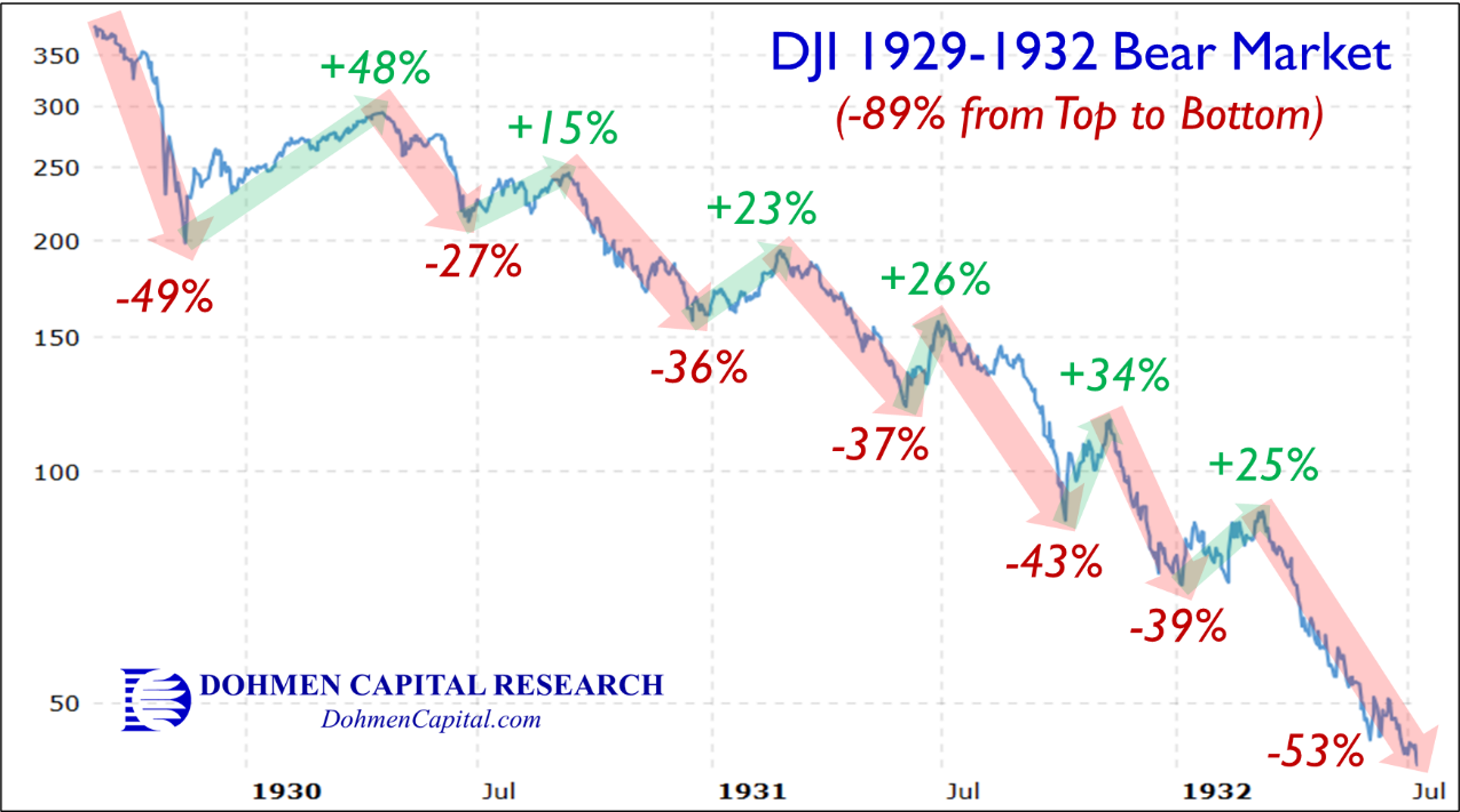

Our friends at Bob Prechter’s Elliott Wave point out that in the bear market of 1929, in which the DJI lost 89%, there were five rallies of more than 20%.

In fact, the chart below of the DJI shows that from the low of 1929 to the high of the next year, 1930, there was a rally of 48% before the bear market resumed. Astounding, but it was still within a bear market.

You see how so many falsehoods are used to sway investors?

In 1930, the biggest names of Wall Street and the economic establishment, such as Maynard Keynes and Irving Fisher, turned very bullish just at the wrong time, near the top of the first bear market rally, which was up 48% from the first crash bottom.

As the Elliott Wave analysts point out, the celebration in 1930 included hit songs, such as “Happy Days are here again.” From that rally high, the DJI plunged over 80%. See the chart below of the DJI 1929-1932 Bear Market with each plunge and ensuing rally.

You can see on the chart below that the 48% up-move from late 1929 to early 1930 was not the start of a “new bull market.”

As it is easy to see, a rally of 20% from a low is no guarantee of a new bull market.

Be assured, this is NOT a new bull market. New definitions don’t change that. The definition given by the financial media about a “20%+ rise” is arbitrary and irrelevant.

We read about an interesting rule from a good analyst at B of A., Savita Subramanian. She has a “Rule of 20” that claims to have a perfect track record: It says that at a bear market bottom, the sum of CPI year-over-year + trailing P/E, has always been lower than 20.

That has not happened yet in this bear market, and therefore, her rule says we have not seen the bottom.

And so, as the chart below shows, while we have seen the combination fall (as inflation has slowed), it remains well above 20 (currently around 24.2).

For it to go below 20, inflation must drop to 0%, which is unlikely, or the P/E ratios of stocks must decline substantially, which would be what happens in big bear markets (chart via Zerohedge).

The negatives for the stock market later this year are plentiful. One is the drastic decline in lending, in addition to the doubling or tripling of interest rates on existing loans.

The highs of the bull market in late 2021 were set when interest rates were low, loans were easy to get, and speculative enthusiasm was at record highs.

Now we have the opposite. However, over the near term, organized manipulation such as organized short squeezes can overcome those fundamentals.

OUR FORECAST

Our outlook at this time is broken down into two important phases over the next 1.5 years. We have written in our award-winning Wellington Letter that at the top of this rally, whenever it occurs, at least one index would make a brief new all-time high.

That would be followed by a potentially sharp market decline starting in the Fall of this year to be followed by a recovery next year ahead of the election. Of course, that is subject to change if the Fed changes their policy.

A bull might say that all the excesses in the markets were wrung out of the market during the decline from November 2021 to October 2022, and therefore, a new bull market now is appropriate.

But bear markets don’t usually end the way they did in October last year, i.e. with a whimper. Usually, it ends with fear.

A meaningful plunge in the market later this year would be likely as it would set the stage for another liquidity boost by the Fed to produce another temporary bear market bottom.

That is what the Fed and other major central banks did after the March 2020 Covid crash. It worked and produced an 18-month speculative frenzy.

The one factor that will enable the Fed in producing a good stock market next year is Artificial Intelligence, AI. The likelihood of a broad speculative frenzy some time ahead in this exciting area is very high.

China will have the greatest number of winners, with the US having some of the large tech firms the winners. China has an army of smart AI experts compared to the US. China will win the AI battle, while the US techies will be experts on “wokism.”

We believe the advent of AI will be the greatest opportunity for investors since the dotcom bubble. Many millionaires and billionaires will be created. But the neophytes must be very cautious and learn to go against their emotions.

But active investors must know how to pick the right stocks, using risk management to survive sharp corrections.

Those who only use US stocks must do their homework to find out which firms have the most capable and largest teams in this field with the most enlightened management. Don’t expect the free financial media to do the work for you.

The period of frantic AI speculation next year will then lead to the monumental crisis that we and some others had expected this year. Risk control will be essential.

Wishing you successful investing

Bert Dohmen

Founder, Dohmen Capital Research

P.S. To learn about the opportunities we see in the market over the next 18 months, read our latest award-winning Wellington Letter, titled “The Last Hurrah?” (published July 30th) by signing up today at DohmenCapital.com.

Members gain instant access to our latest issue along with our 5 most recent issues, including the important issue from July 12th titled “The Unacknowledged Recession”.