It appears that the big, smart money worldwide is scrambling to buy TRILLIONS of dollars of bonds, even bonds with negative yields. Inflows into bond funds are near a record high. Global bond funds have had an inflow of about $330 billion just this year. That is huge.

Normally, we would consider such massive buying a bearish sign as it could be a sign of excessive enthusiasm. But this time it gets so little attention. There is no sign of great public enthusiasm.

Globally, there are now over $13 TRILLION of bonds with yields not just at zero but below, i.e., negative. That is double the amount of what it was last December. Why would these huge bond buyers pay to own a bond instead of receiving interest? Read on.

Furthermore, in spite of this huge but quiet rush into bonds, analysts in the media have not hyped or even mentioned bonds as a great investment. We consider that very bullish.

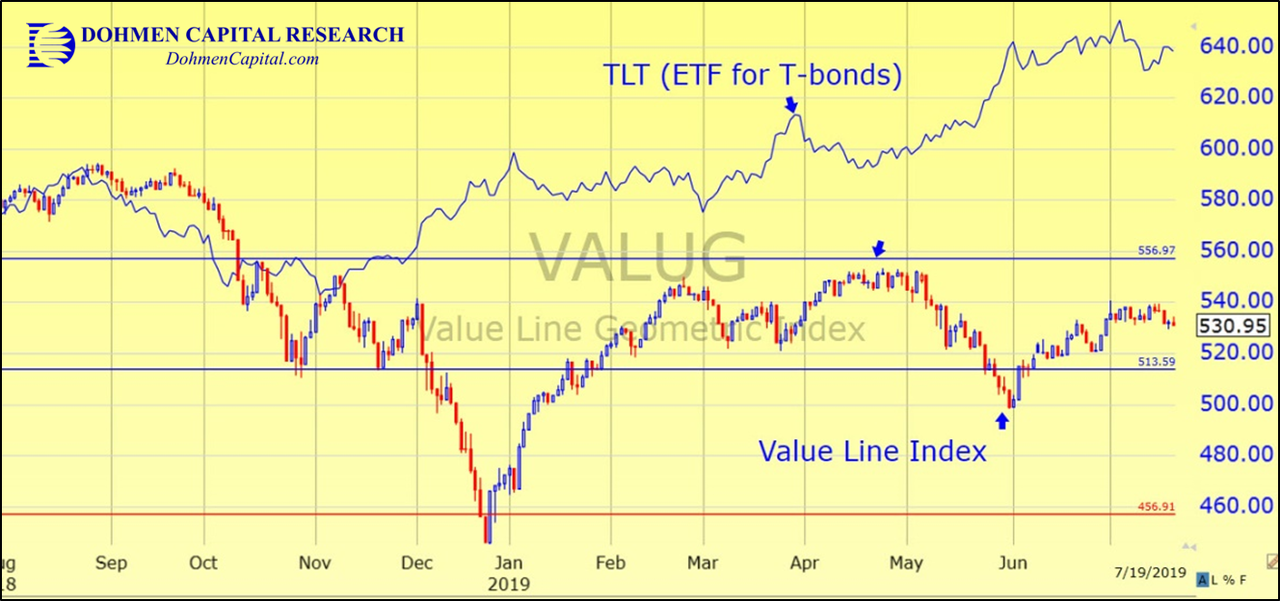

It’s even more amazing that although bonds have outperformed stocks the past 1-2 years, we believe the inflows reflect “smart money.” Here is the chart of the very broad Value Line Index (VALUG), which represents the true stock market, vs. the ETF for long-term T-bonds.

There is more about the urge to get into bonds, not just the yield. In fact, one-third of all European investment-grade bonds, and a third of 2-year European bonds rated “junk,” yield less than zero.

Now there are 14 junk-bond issues globally with yields below zero. That’s incredible. Negative bond yields can be defended for safe AAA bonds. But junk bonds with no backing can’t be considered a “safe haven.” No one is thinking about how all this will eventually end. Our conclusion: Badly!

Imagine hundreds of billions of dollars going into bonds with no yield, and even negative yield, where the buyer pays interest for the privilege of holding that junk. Why would anyone do this?

Two reasons:

- The bonds, especially the IG (investment grade), are considered safer than the banks.

- The anticipation that bond yields will go even lower, signifying a big rise in bond prices.

We have not heard one analyst mention the latter. Do they think that is too deep for average investors to understand? Well, our valued members get it.

Take the 100-year Austrian bond issued two years ago. It has soared 60% in that time as its yield dropped from 2.1% to 1.2%.

Now Austria is considering issuing another tranche of the 100-year bond.

And that is what is driving the global bond market rally: expectations of recessions, perhaps deep ones, and a scramble for bonds, driving their yields down and their prices higher.

The world has gone upside down. How can this possibly have a good ending? Whenever these yields “normalize,” i.e. rise to historical levels, whether it is next year or 10 years from now, the bond markets will plunge. Bonds could lose 50% or more of their value. It’s mathematical!

Countries are now able to issue 100-year bonds at very low yields. Imagine lending your money to Argentina for 100 years!

In the past, normal investment prudence never would have made negative-yielding bonds possible. There would have been no buyers. So we ask, why are money managers buying now?

We explain this incredibly under-the-radar story in our latest Wellington Letter.

Since 1977, our flagship investment newsletter has provided readers with independent and unconflicted investment research along with our easy-to-understand analysis of the global economies and investment markets.

Serious investors can read our latest macro view of the major global markets as we sort out the noise from the truly important news and factors impacting their investments.

Wishing you good health and prosperous investing,

Bert Dohmen, Founder

Dohmen Capital Research

Dohmen Strategies, LLC